Seaweed Supply Chains: Inside Fifty-Years of Industrial Cultivation

INVESTIGATING THE SCIENTIFIC BREAKTHROUGHS AND CAPITAL FLOWS THAT TRANSFORMED A FORAGED WILD RESOURCE INTO A $20BN GLOBAL COMMODITY

I. PREDICTABILITY IN THE WILD: KELCO'S 1978 EXIT

The origins of today's cultivated seaweed supply are rooted in a foundational supply problem of the late 1970s. In our last post, we described how Kelco, then a dominant force in alginate production, abandoned its dependence on wild kelp. The rationale was simple: supply was fundamentally unbankable. Harvests were consistently subject to weather volatility—storms were a primary source of disruption—and biological cycles that defied industrial scheduling. The weather-dependent feedstock proved incapable of supporting industrial-scale customer requirements, prompting the company to pivot to a microbial monoculture.

In 1978, in the absence of a viable cultivated alternative, the decision to seek control through a fermenter—to master chemistry over unreliable biology—was a sound one for capital markets. Nonetheless, the industrialization of the seaweed supply chain was by then already underway. This inquiry examines the fifty-year trajectory of the supply chain since Kelco’s exit.

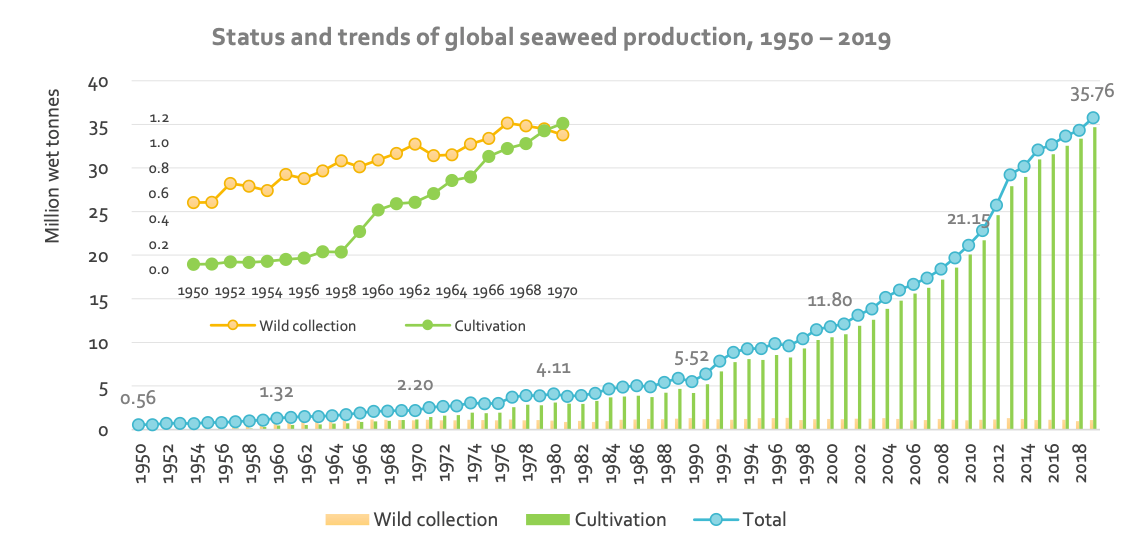

II. THE EMERGENCE OF A GLOBAL COMMODITY

Data source: FAO Global Fishery and Aquaculture Production Statistics (FishStatJ)

Five decades later, the cultivated supply model is not only extant but dominant. As of 2019, global production of aquatic plants—overwhelmingly seaweeds—reached 35.8 million wet tonnes, with cultivation accounting for a commanding 97% of that volume1. The supply volatility that forced Kelco's exit is now a marginal factor against a cultivated base that grew a thousand-fold between 1950 and 2019, from 34,700 tonnes to 34.7 million.1

The sector's scale is underpinned by five primary species groups that collectively represent over 95 per cent of global cultivated tonnage:

● Laminaria/Saccharina (kombu kelps) at 12.3 million tonnes.

● Carrageenan-bearing reds (Kappaphycus and Eucheuma) at 11.6 million tonnes.

● Gracilaria (agar) at 3.6 million tonnes.

● Porphyra/Pyropia (nori) at 3.0 million tonnes.

● Undaria (wakame) at 2.6 million tonnes.

This industrial base is multi-jurisdictional, mitigating single-source risk. China leads with 56.8 per cent of production, followed by Indonesia (27.9%), Korea (5.1%), the Philippines (4.2%), and Japan (1.2%).1

The market scale mirrors the volume, with global seaweed cultivation valued at approximately $20 billion in 2025, and projections targeting $33 billion by 2030.2 Significantly, Korean exports alone breached the $1 billion mark in 2025, a 13% year-over-year increase. What began as a regional food source is now a globally traded, liquid ingredient category.

NASA satellite image of seaweed farms in Wando County, South Korea. February 19, 2021.

III. CULTIVATION: THE INFRASTRUCTURE OF INDUSTRIAL SCALE

The exponential increase in tonnage was not serendipitous. It is the result of scientific and methodological breakthroughs, each transforming a volatile wild resource into a predictable farmed feedstock. Here are three transformative advances in the cultivation of seaweed:

1. The Nori Supply Chain De-risked (1949)

Memorial to Drew-Baker in Uto City, Japan.

The first critical advancement in seaweed domestication was the seashell seeding of Porphyra (nori). Before this, the post-war Japanese nori industry faced collapse due to the failure of wild seed sources. In 1949, British phycologist Kathleen Drew-Baker identified the conchocelis stage—the previously unconnected filamentous, shell-boring half of the life cycle.3 Her discovery enabled the culture of conchocelis on oyster shells in controlled tanks, allowing sporulation on demand and reliable seeding onto grow-out nets. This scientific clarity provided the foundation for Japan to rebuild its industry, which Korea and China subsequently industrialized.4 Drew-Baker’s intervention is commemorated every April 14 in Japan, where she is known as the Mother of the Sea, and the method now underpins roughly 3 million tonnes of annual production.1

2. Engineering Kelp Gametophytes for Mass Production (1955)

Image credit: Jaclyn Robidoux, Maine Sea Grant

The second breakthrough introduced the kelp gametophyte hatchery with twine-seeded sporelings. Kelp species like Saccharina japonicaand Undaria pinnatifida are now cultivated through a closed, controlled hatchery protocol. This involves holding haploid gametophyte cultures under specific light to suppress reproduction, inducing fertilization in tanks, and allowing microscopic sporophytes to settle on cotton twine.4 The key work was executed by Chinese phycologist C. K. Tseng, who developed summer sporophyte seedling-raising and floating-raft cultivation in 1955, followed by Fang Zongxi's intra-specific cross-breeding protocols in 1963.5 Their work converted Saccharina japonica from a regional Japanese specialty to a global industrial crop, now responsible for approximately 12 million tonnes annually. This fundamental gametophyte-and-twine workflow is the same technology now being scaled by North American kelp hatcheries.

3. The Off-Bottom Monoline for Carrageenan (1970s)

Kappaphycus alvarezii cultivation using off-bottom monoline farming. Zanzibar, Tanzania.

The third method secured the tropical red supply: the off-bottom monoline. In the early 1970s, American phycologist Maxwell Doty, collaborating with the U.S.-based Marine Colloids, successfully transferred Kappaphycus alvarezii from Hawaii to the southern Philippines. The first commercial farm, based on cultivation on monolines tied between bamboo stakes in shallow lagoons, was established at Tawi-Tawi in 1969.6 This scalable, accessible method was adopted by smallholders across the Philippines, Indonesia, and Tanzania, establishing the global carrageenan supply chain.7Kappaphycus and Eucheuma are now a significant category in seaweed aquaculture, producing roughly 11.6 million tonnes annually.

The critical difference between 1978 and today is encapsulated in these three developments: methods that converted a variable wild resource into a predictable, farmable feedstock are now fully operational.

IV. THE INSTITUTIONAL MANDATE AND CAPITAL FLOW

The existing tonnage provides the foundation, but the momentum for the next chapter is driven by institutional alignment and dedicated capital.

In 2023, the World Bank and Hatch Blue quantified the sector’s expansion potential, identifying ten non-traditional applications—including biostimulants, methane-reducing feed additives, nutraceuticals, and ecosystem-service credits—with a combined incremental market potential of up to $11.8 billion by 2030.8 This explicit valuation by a major financial institution signals the sector's graduation from niche production to a serious global investment thesis.

Simultaneously, the necessary infrastructure for supply chain integrity is being solidified. The UN Global Compact and Lloyd's Register Foundation published the Seaweed Manifesto in 20209, leading to the 2021 launch of the Global Seaweed Coalition (formerly the Safe Seaweed Coalition).10 This coalition is focused on establishing and coordinating standards for consumer, environmental, and operational safety across the value chain. Institutions are essential for de-risking the commodity and allowing global brands to source at scale.

Capital has followed at multiple scales. Venture investment into blue-economy startups reached roughly $2.4 billion in 2024, a tenfold increase on prior years11. Cumulative private capital deployed into seaweed ventures specifically has passed $780 million by 2026, according to the investment tracker maintained by Phyconomy12. Flagship rounds include Notpla's £20 million raise for seaweed-based packaging, Ocean Rainforest's $6.2 million Series A led by Builders Vision, and grant-stacked equity at specialist firms including Symbrosia, Sway, and Umaro Foods14.

V. THE FORWARD CAPACITY PIPELINE

Kelp farming in south eastern Alaska.

While the headline figures detail current production, the next decade of capacity is already moving through development cycles—across nurseries, deep-water trials, and cultivar improvement programs.

Korea's Dual Bet: South Korea is committing to parallel expansion strategies, approving approximately 1,000 hectares of sea space for deep-water trials and allocating around $25 million to commercially scale land-based gim (nori) farming by 2029.2 These two bets are a significant commitment from the source of the world's most internationally-traded seaweed exports.

North American Maturation: The kelp buildout in North America has achieved commercial scale, demonstrated by GreenWave's 2026 report, which catalogs 249 permitted kelp farms covering 6,280 acres. Production is currently focused in Alaska and the U.S. Northeast.15The regulatory and permitting infrastructure, largely absent in 2015, is now mature across multiple jurisdictions, facilitating the launch of new regional value chains.

Advanced seaweed bioreactors developed and sold by Industrial Plankton.

The Yield Lever: Cultivar Improvement: The most potent lever on future yield is continuous improvement in hatchery science. Western hatcheries utilizing the gametophyte-and-twine workflow are scaling output, making the techno-economic case for industrial-scale kelp nurseries viable for capital investment.15 Concurrently, Asian research efforts are driving cultivar improvement through marker-assisted breeding for enhanced Saccharina yield and resistance to diseases like Kappaphycus ice-ice.5

This capacity expansion is not speculative: hectares are permitted, capital is committed, and improved cultivars are in selection, ensuring continued growth on top of the already substantial base.

VI. INVESTMENT IMPLICATIONS

For stakeholders developing food, agricultural, or material products predicated on seaweed-derived inputs, the supply narrative has fundamentally shifted. The current supply chain is defined by cultivation, multi-species and multi-jurisdictional redundancy, robust methodologies, institutional backing, committed capital, and a clear trajectory for expansion.

The 1978 decision by Kelco to divest from kelp was justifiable for its time, dictated by the unreliability of wild supply. The correct investment thesis for 2026 is based on the opposite reality: the scientific and commercial infrastructure that was absent then is now in place, and the market trajectory points upward.

The integrity of the ingredient and the security of its supply chain are now co-evolving. The advantage in the next decade will accrue to those who treat both as equally serious investment targets.

SOURCES

1. Cai, J. (FAO, 2021). Global status of seaweed production, trade and utilization. Seaweed Innovation Forum Belize, 28 May 2021. Data: FAO Global Fishery and Aquaculture Production Statistics (FishStatJ), March 2021. https://www.competecaribbean.org/wp-content/uploads/2021/05/Global-status-of-seaweed-production-trade-and-utilization-Junning-Cai-FAO.pdf

2. Hermans, S. (2026). Seaweed in 2025: the year in review. Phyconomy. https://phyconomy.substack.com/p/seaweed-in-2025-the-year-in-review

3. Drew, K. M. (1949). Conchocelis-phase in the life-history of Porphyra umbilicalis (L.) Kütz. Nature 164:748–749. https://www.nature.com/articles/164748a0

4. Buschmann, A. H., Camus, C., Infante, J., Neori, A., Israel, Á., Hernández-González, M. C., Pereda, S. V., Gómez-Pinchetti, J. L., Golberg, A., Tadmor-Shalev, N., Critchley, A. T. (2017). Seaweed production: overview of the global state of exploitation, farming and emerging research activity. European Journal of Phycology 52(4):391–406. https://www.tandfonline.com/doi/full/10.1080/09670262.2017.1365175

5. Hu, Z.-M., Shan, T.-F., Zhang, Q.-S., Liu, F.-L., Jueterbock, A., Wang, X.-Y., Sun, Z.-M., Wang, J.-J., Hu, X.-Q., Bi, Y.-H., Mao, Y.-X., Choi, H.-G., Duan, D.-L. (2021). Kelp aquaculture in China: a retrospective and future prospects. Reviews in Aquaculture 13(3):1324–1351. https://onlinelibrary.wiley.com/doi/10.1111/raq.12524

6. Hurtado, A. Q., Gerung, G. S., Yasir, S., Critchley, A. T. (2014). Developments in production technology of Kappaphycus in the Philippines: more than four decades of farming. Journal of Applied Phycology 26:1945–1961. https://link.springer.com/article/10.1007/s10811-014-0510-4

7. Bixler, H. J., Porse, H. (2011). A decade of change in the seaweed hydrocolloids industry. Journal of Applied Phycology 23:321–335. https://link.springer.com/article/10.1007/s10811-010-9529-3

8. World Bank Group and Hatch Blue (2023). Global Seaweed: New and Emerging Markets Report 2023. https://www.worldbank.org/en/topic/environment/publication/global-seaweed-new-and-emerging-markets-report-2023

9. UN Global Compact and Lloyd's Register Foundation (2020). Seaweed Manifesto. https://unglobalcompact.org/library/5743

10. Global Seaweed Coalition (formerly Safe Seaweed Coalition), founded 2021 by UN Global Compact, Lloyd's Register Foundation, and CNRS. https://www.safeseaweedcoalition.org/about-us/

11. Environment Next (2025). Riding the Blue Wave: The Rise of Ocean-Focused Venture Capital. https://environmentnext.org/riding-the-blue-wave-the-rise-of-ocean-focused-venture-capital/

12. Time (2026). A New Wave of Investors Sees Profit in Ocean Conservation. 28 May 2026. https://time.com/article/2026/05/28/the-new-value-of-oceans/

13. The Fish Site (2023). Seaweed packaging startup Notpla secures £20 million investment. https://thefishsite.com/articles/seaweed-packaging-startup-notpla-secures-20-million-investment

14. The Fish Site (2024). Sway and Umaro secure $1.5 million DOE MACRO grant. https://thefishsite.com/articles/sway-and-umaro-secure-1-5-million-grant

15. GreenWave (2026). State of the Kelp Industry: A Decade in Review and the Road Ahead. https://www.greenwave.org/report